A Report on Hedging, Speculation, and Income Generation

A Report on Hedging, Speculation, and Income Generation for Options, ETOs, Trading, Premium selling and risk management

Options contracts are the most versatile assets available. Not only do they benefit from price change, they are also exposed to "extrinsic value" components such as time decay and Implied Volatility. This creates vast amounts of flexibility for use cases of these derivatives.

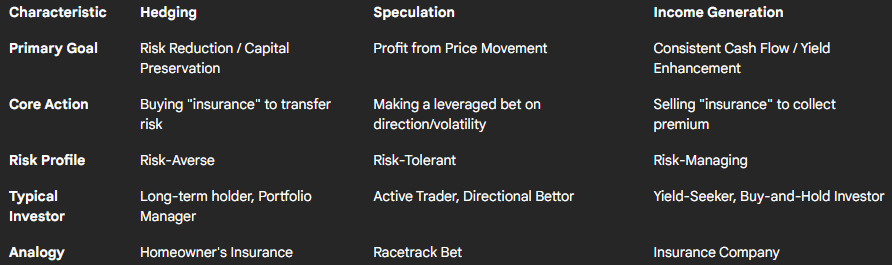

The utility of options is best understood through their three primary uses: hedging, speculation, and income generation.

Hedging uses options to protect existing assets against adverse price movements.

Speculation employs the inherent leverage of options to make directional bets on an asset's future price, seeking high returns in exchange for defined risk.

Income generation involves selling options to collect the premium, with the idea of extracting the time value over the life of the contracts.

Traders gain exposure for many reasons. The demand from hedgers and speculators creates a market for options, which is met by income-focused investors who sell contracts and collect premiums for assuming risk. This creates the exchange traded market and liquidity to exchange derivatives in the marketplace.

Revisiting Options. What are they?

An options contract gives the buyer the right, not the obligation, to transact an underlying security at a set price by a specific date. The options seller (or writer), has the obligation to fulfil that contract should it be exercised. Buyers pay a premium and writers receive the premium as the agreement is established.

All strategies use two basic contract types: calls and puts.

- Call Options: Gives the holder the right to buy an asset at a specified price. Call buyers are bullish. The seller has the obligation to sell the asset if the option is exercised.

- Put Options: Gives the holder the right to sell an asset at a specified price. Put buyers are bearish. The seller is obligated to buy the asset if exercised.

Contract terms are standardized for exchange trading:

- Underlying Asset: The security (stock, ETF) the contract pertains to, typically representing 100 shares.

- Strike (Exercise) Price: The fixed and agreed price for the transaction if the option is exercised.

- Expiration Date: The final day the option can be exercised, after which it becomes void.

An option's premium consists of two components: intrinsic and extrinsic value. Understanding this is vital for selecting the right option.

- Intrinsic Value: The tangible value if exercised immediately, or the amount an option is "in-the-money" (ITM). For a call, it's the stock price minus the strike price (if positive). For a put, it's the strike price minus the stock price (if positive). It cannot be negative.

- Extrinsic Value (Time Value): The premium amount exceeding intrinsic value, representing the chance the option could become more valuable. It is primarily influenced by time to expiration (more time equals more value) and implied volatility (higher IV equals more value).

This leads to the concept of Moneyness, which describes the strike price relative to the stock price :

- In-the-Money (ITM): An option with intrinsic value.

- At-the-Money (ATM): Strike price is very close to the stock price.

- Out-of-the-Money (OTM): An option with zero intrinsic value.

Hedging: Insuring Against Market Uncertainty

Hedging is a conservative use of options for risk management and capital preservation, generally not to profit. The goal is to protect an asset or portfolio from adverse price moves, similar to buying insurance. The typical hedger is a risk-averse, long-term investor or portfolio manager looking to protect unrealized gains without liquidating a position.

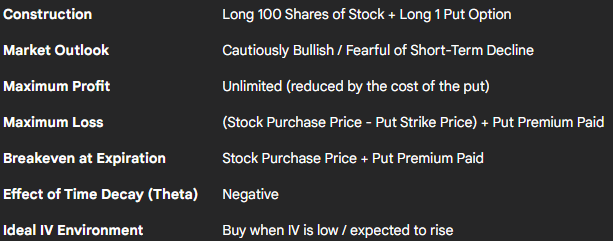

Primary Strategy: The Protective Put.

- Mechanics: This involves owning an underlying stock and purchasing one put option on that same stock. If done simultaneously, it's a "married put".

- Strategic Application: The put option acts as an insurance policy, establishing a "floor" price (the strike price) below which the position's value cannot fall, capping losses.

- Market Conditions: Ideal for an investor who is long-term bullish but fears a short-term risk, such as a market correction or a specific event like an earnings announcement.

- Trade-offs: The cost of the put premium reduces total profit if the stock appreciates. If the stock rises or stays flat, the put expires worthless, and the premium is a sunk cost.

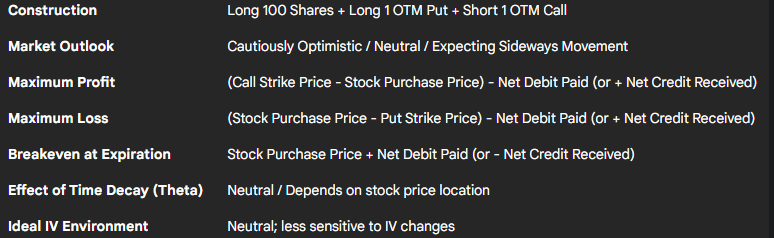

Advanced Hedging: The Collar

A collar offers downside protection similar to a protective put but at a reduced or even zero cost.

- Mechanics: A collar combines a long stock position with a long out-of-the-money (OTM) protective put and a short OTM call. The long put protects a downside move, while the short call creates an upside ceiling.

- Strategic Application: The premium collected from selling the call is used to offset or cover the cost of buying the put. A "zero-cost collar" offers downside protection for no net outlay, where the premium received from selling the call option pays for the price of the put option, making it an efficient way to hedge.

- Market Conditions: Best when an investor is cautiously optimistic or expects the stock to trade sideways. It is suboptimal in a strong bull market, as gains are capped if the stock is called away.

- Trade-offs: The critical trade-off is forfeiting upside potential above the short call's strike price in exchange for cheap or free downside insurance.

Speculation: Leveraging a Market Thesis

Options speculation involves taking on defined risk to pursue amplified returns. Options are preferred for their inherent leverage, which allows control over a large stock position for a fraction of the upfront cost. The speculator aims to profit from a strong, time-sensitive thesis about an asset's price direction.

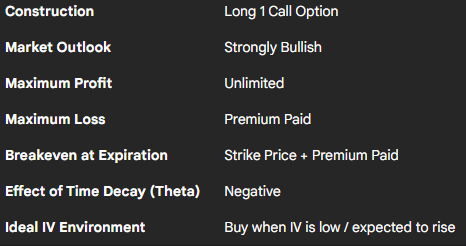

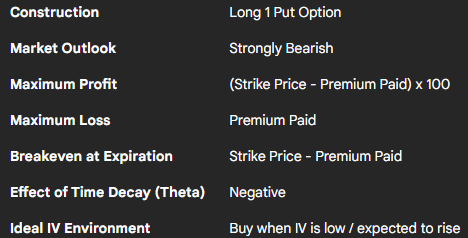

Directional Strategy: Long Calls and Long Puts

Strategy Profile: Long Call

Strategy Profile: Long Put

- Mechanics: A bullish investor buys a call option; a bearish investor buys a put option.

- Strategic Application: The goal is leveraged returns. A small percentage increase in a stock's price can result in a much larger percentage gain on the option's premium, with risk strictly limited to the premium paid.

- Market Conditions: Best used with strong conviction on both the direction and timing of a price move. Time decay is a constant headwind, so the move must happen within the contracts timeframe.

- Trade-offs: While risk is limited, the probability of profit is often low. The stock must move enough to cover the premium before seeing profit. Often seen as a high-risk high-reward trading style. This however can be altered by how you structure your trade to begin with and what option series you decide to buy.

Income Generation: Selling Premium

Income generation with options involves selling options to collect a premium, acting like an insurance provider. The goal is for the sold options to expire worthless, so the trader collects and keeps the premium, with no obligation.

Think about how many months you've paid your monthly insurance payments, vs the amount of times you've called on them for help.

The best part is the trader gets to decide how much risk to take, on what asset class and for how long, having complete flexibility of what position to be in at any time.

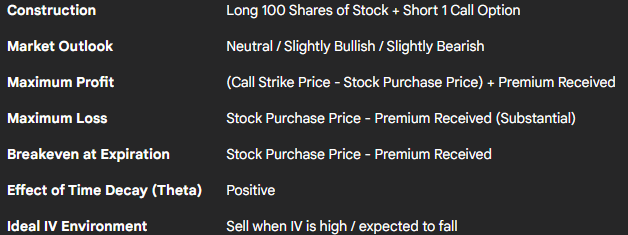

The Covered Call

- Mechanics: An investor owning at least 100 shares of a stock sells one call option against that holding. The long stock "covers" the short call's obligation, avoiding the unlimited risk of a naked call.

- Strategic Application: The primary use is to generate income (the premium) from an existing stock holding. It can also be used to set a target selling price.

- Market Conditions: Best for neutral or slightly bullish markets. In a sharply rising market, opportunity cost is high as gains are capped. In a falling market, the premium offers only a small cushion against losses.

- Trade-offs: The principal trade-off is capped upside potential above the call's strike price, potentially missing out on excess stock gains.

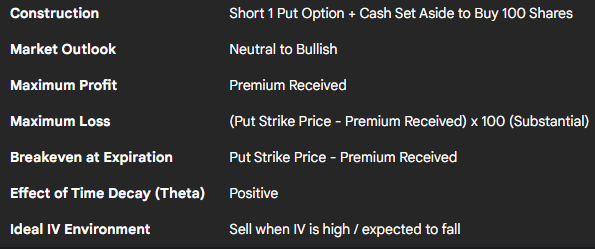

The Cash-Secured Put

- Mechanics: An investor sells a put option and sets aside enough cash to purchase 100 shares at the strike price if assigned. This cash collateral "secures" the put.

- Strategic Application: This is a dual-purpose strategy: generate income from the premium, and potentially acquire a desired stock at an effective price lower than the current market price (strike price minus premium received).

- Market Conditions: Best in neutral-to-bullish markets. The ideal outcome is for the stock to remain above the strike, letting the put expire worthless.

- Trade-offs: Profit is limited to the premium received. The primary risk is a sharp decline in the stock, obligating the investor to buy shares at the higher strike price, realizing an immediate paper loss.

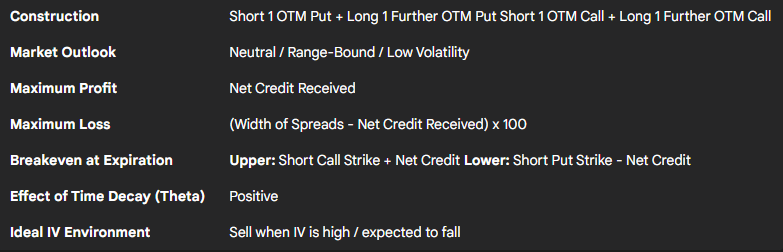

Advanced Income Strategy: The Iron Condor

The iron condor is a non-directional strategy that profits if a stock's price remains within a specific range.

Mechanics: An iron condor combines a bull put spread and a bear call spread, resulting in a double net credit from two credit spreads.

Strategic Application: The goal is to generate income from the expectation that a stock's price will stay between the short put and short call strikes until expiration. The strategy profits from time decay and a decrease in implied volatility.

- Market Conditions: Tailor-made for a range-bound market, It is best initiated when implied volatility is high and is expected to decrease, allowing the investor to sell expensive options and let the premiums erode over time.

- Trade-offs: The iron condor has a high probability of profit but a skewed risk/reward profile. The maximum profit is small (the net credit), while the maximum potential loss is significantly larger, depending on how far OTM the investor structures the trade.

The Business of Selling Premium

Using options for income requires a shift in mindset from traditional investing. The premium seller's profit is capped at the premium collected. Success requires acting as an active risk manager, not a passive investor. The goal is to find situations where the premium (from high implied volatility) overcompensates for the statistical risk. Profitability depends on managing the occasional losses effectively.

Cash-secured-put selling act unusually similar to how an insurance business works. Traders receive payments up front. to then potentially protect an assets value at a later date. Famously, Warren Buffett's Berkshire Hathaway uses this strategy to generate billions of dollars annually by collecting options premiums.

Conclusion

The three uses of options—hedging, speculation, and income generation—are not mutually exclusive. A sophisticated investor might use all three: selling covered calls for income, using that income to buy puts to hedge the portfolio, and using separate capital to speculate with long calls in another sector / asset class.

What's right for you? Hopefully this report provided insight to understanding the power of options and versatile nature of strategy selection. Any thoughts / comments please leave them below.